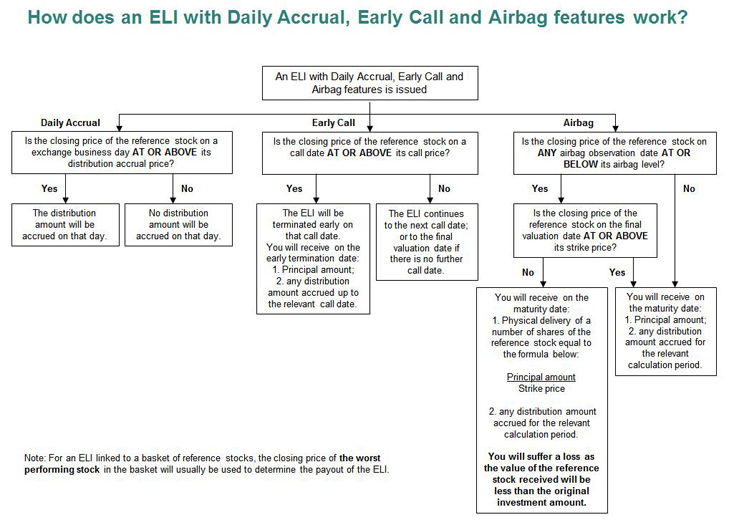

Combined features

Some issuers may combine several special features, such as daily accrual, early call and airbag in their ELIs. The flow-chart below will illustrate how an ELI with combined features works.

|

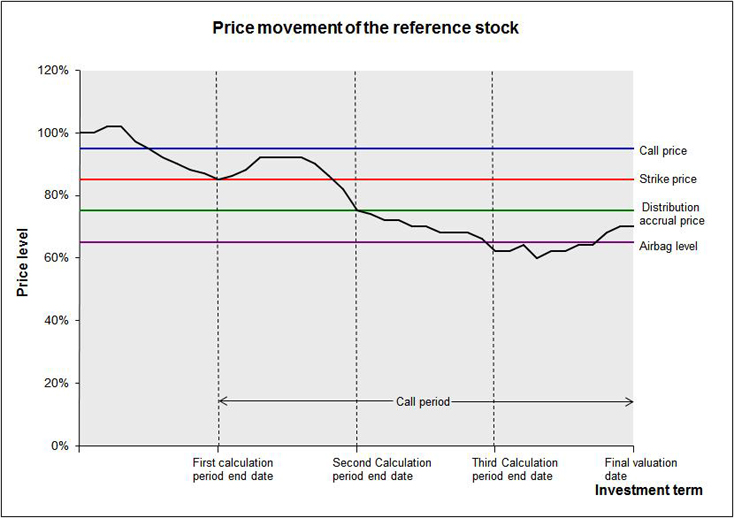

Example (Note 1): Bull ELI with daily accrual, early call and airbag features

| Principal amount | $100,000 |

|---|---|

| Purchase price | $100,000 |

| Strike price | 85% of initial spot price |

| Distribution accrual price | 75% of initial spot price |

| Distribution rate | 3% |

| Distribution amount | Principal amount X distribution rate X (accrued days / total days per calculation period) |

| Accrued days | The number of exchange business days on which the closing price of the reference stock is at or above its distribution accrual price in the relevant calculation period |

| Total days per calculation period | 60 days |

| Call price | 95% of initial spot price |

| Call period | each exchange business day starting from the first calculation period end date (including) up to the final valuation date (excluding) |

| Airbag level | 65% of initial spot price |

| Airbag observation period | each exchange business day starting from the trade date (excluding) to the final valuation date (including) |

|

Based on the assumed price movement of the reference stock as shown in the above diagram, you can expect the following results:

Early Call:

As the reference stock closes below the call price on each exchange business day within the call period, the ELI will not be terminated before maturity.

Distribution amount:

First and second calculation periods:

As the reference stock closes at or above the distribution accrual price on each exchange business day during the first and second calculation periods, you will receive a distribution amount, in this case, $100,000 X 3% X 60 / 60 = $3,000, for each of these calculation periods.

Third and fourth calculation periods:

As the reference stock closes below the distribution accrual price on each exchange business day during the third and fourth calculation periods, you will not receive any distribution amount for the third or fourth calculation period.

Settlement on the maturity date:

As the reference stock closes at or below the airbag level on one or more exchange business days within the airbag observation period, and that it closes at 70% of the initial spot price on the final valuation date, or below the strike price, you will receive a pre-determined number of shares of the reference stock on the maturity date based on the following formula:

Principal amount ÷ Strike price

You should note that if the closing price of the reference stock on any exchange business day within the airbag observation period is at or below its airbag level, you will in effect be obligated to buy the reference stock at its strike price, if the closing price of the reference stock on the final valuation date is below its strike price. In this case you will suffer a loss as the value of the shares delivered to you will be less (or substantially less) than your original investment amount. In an extreme case, you could lose the entire amount invested.

You should NOT buy an ELI with special features if you do not fully understand the features and the risks of the product. Seek professional advice first.

Note 1:Please note that the example shown above is for illustration only and the actual terms will vary for different products.