A tricky derivative for the market's ups and downs

By Alan Alanson

One of the most popular investment products in Hong Kong is the CBBC - the callable bull/bear contract. This is something you can buy online like you would buy stocks. But it is not a share nor a bond. It is a derivative contract.

One of the most popular investment products in Hong Kong is the CBBC - the callable bull/bear contract. This is something you can buy online like you would buy stocks. But it is not a share nor a bond. It is a derivative contract.

A CBBC is similar to a warrant, an option or a forward contract - not really an asset in the conventional sense of the word, but a contract that you can buy and sell. Its value is determined, among other things, by the performance of an asset it is linked to. And the asset that most CBBCs traded in Hong Kong are linked to is the Hang Seng Index.

The bull/bear part describes two different products that can also be called a callable bull contract and a callable bear contract. A HSI callable bull contract rises in value if the index rises and a HSI callable bear contract rises in value if it falls.

The callable part is one of the key things that sets a CBBC apart from similar derivative products such as warrants. If the value of the underlying asset hits a predetermined call price, the bank that issued it gets to call the CBBC. That means the holder of the CBBC has to give it back to the issuer and the contract is over, the CBBC is gone.

If you think the HSI will rise, you might buy a callable bull contract. If the HSI rises, you should be able to sell it at a profit. But if the HSI falls, the CBBC's value will also drop, giving you the option to sell it and take the loss, or perhaps hold on in the hope that the HSI will recover.

But if the CBBC has a call price of say 11,000 and the HSI falls to 11,000, you no longer have the option of holding onto the contract. Instead, the issuer will call it back and you will have lost your investment.

CBBCs also have a number of other important features that need to be understood if you want to buy them. These are: spot price, strike price, finance cost, expiry date, entitlement ratio and underlying asset.

Spot price is what it actually costs to buy or sell the CBBC. The strike price is a bit more confusing. It is linked to the concept of residual value. The residual value is what the CBBC is worth after it is called. So in our example, if the call price is 11,000 and the HSI falls to 11,000, the CBBC will be called. But if the strike price is 10,000, the CBBC may have some residual value. This is because the residual value is calculated on the basis of the strike price, not the call price. The call price tells you when it will be called and the strike price tells you what it is worth when it is called.

The finance cost is a charge that gets added to the CBBC's spot price. It covers the issuer's costs for creating the CBBC and varies from time to time, tending to decrease the closer the CBBC gets to its expiry date.

The expiry date is the end of the life of the CBBC, and at that time the residual value is calculated by reference to the strike price.

The entitlement ratio represents the CBBC's exposure to the underlying asset. If this ratio is 10, you would need to buy 10 CBBCs to have one-to-one exposure to the underlying asset. If the underlying asset is a share that is worth HK$200 and the strike price of a bull CBBC is HK$100, the value of the CBBC is basically the difference, or HK$100. If the entitlement ratio is 1, the CBBC would be worth HK$100. If the entitlement ratio is 100, the CBBC is worth HK$1, if it is 1,000, then HK$0.10, and so on.

Assume you buy a callable bull contract with the HSI as the underlying asset. Say the HSI is at 15,000 at the time of buying it, the strike price is 10,000, the call price is 11,000, the finance cost per CBBC is HK$0.01 and the entitlement ratio is 10,000.

Assume you buy a callable bull contract with the HSI as the underlying asset. Say the HSI is at 15,000 at the time of buying it, the strike price is 10,000, the call price is 11,000, the finance cost per CBBC is HK$0.01 and the entitlement ratio is 10,000.

As this is a bull contract, you would buy it if you anticipate the HSI is going to rise. If the HSI is at 15,000 when you buy the CBBC, it s value would be 15,000 less the strike price, divided by the entitlement ratio, plus the finance cost.

Example: Callable bull contract

Underlying contract: Hang Seng Index Value of HSI at time of purchase of contract: 15,000 Strike price: 10,000 Call price: 11,000 Finance cost (per CBBC): HK$0.01 Entitlement ratio: 10,000 CBBC value: HK$0.51

| Underlying contract: | Hang Seng Index | |

| Value of HSI at time of purchase of contract: | 15,000 | |

| Strike price: | 10,000 | |

| Call price: | 11,000 | |

| Finance cost (per CBBC): | HK$0.01 | |

| Entitlement ratio: | 10,000 | |

| CBBC value: HK$0.51 |

That works out to be HK$0.51 - that is what this CBBC is worth when you buy it. That does not of course mean you can go buy one for HK$0.51. There will be minimum number you need to buy, called a board lot, of 10,000 say. But still, the entry price if you just buy one board lot on this imaginary CBBC is a relatively small HK$5,100.

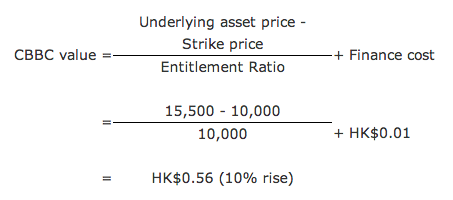

Generally investors will only hold CBBCs for a very short time. They can be bought and sold on the market and a common strategy is to buy a bull CBBC, wait until it increases in value and then sell it. On a single day, for example, the HSI could easily rise 500 points. If the index goes from 15,000 to 15,500, this 3 per cent gain on the index would translate into an almost 10 per cent gain in the value of our hypothetical CBBC using the formula to calculate the CBBC's price.

Example: if HSI gain 3%

But of course this works fine if the HSI does increase in value.

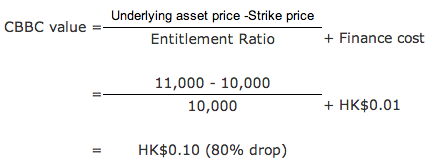

In the same way that percentage increases in the value of the CBBC are greater than percentage increases in the value of the HSI, so are losses. Imagine, the index does not rise and you do not get the chance to sell for a profit. If things go badly and the HSI drops, the contract will be called and you will receive the residual value - generally difference between the call price and the strike price.

Say the HSI drops 4,000 points, or 27 per cent. Using the same formula, your CBBC has dropped 80 per cent from HK$0.51 to HK$0.10.

Example: if HSI drops 27%

Now, if you think the HSI is going to drop you buy a bear CBBC. If the index is at 15,000, the value of a bear CBBC is its strike price less 15,000, plus finance costs. So the lower the index goes, the greater the value of the contract. Just like with a bull CBBC, if the index moves in the wrong direction, which in the case of a bear CBBC would be upwards, the bear CBBC loses value. If the index moves upwards for long enough, the contract will be called and you may be left with some residual value.

One slight twist in the calculation of the residual value is that although the contract will be called if the index reaches the call price, the residual value is not calculated immediately. In the case of a bull contract, the underlying asset price used to calculate the residual value is the lowest value of the asset in the trading session during which the CBBC is called and in the following session.

So in our bull CBBC, if it is called when the HSI is at 11,000, but later that day it hits 9,900, the residual value will be zero. It is not like an accumulator - a CBBC will not be worth less than zero so you will never lose more that you have invested. But the residual value can evaporate if the market continues to move in the wrong direction.

Bear in mind I am using a theoretical CBBC to illustrate how these things work. The actual world of CBBCs is a bit more complicated. For every underlying asset, particularly in the case of the most popular underlying assets like the HSI, there are loads of different CBBCs to choose from.

In our example of a CBBC linked to the HSI with a strike price of 10,000 and a hypothetical index price of 15,000, a 3 per cent change in the index translates into a 10 per cent gain in this CBBC's value.

Now, if the strike price is much closer to the index value, say 14,000, the changes in value are even further magnified. In the above bull CBBC example, if the index is at 15,000 and the CBBC has a strike price of 14,000, it will be worth HK$0.11. If the index rises to 15,500, the CBBC will be worth HK$0.16. A 3 per cent rise in the value of the HSI would translate into a 45 per cent rise in this CBBC's value.

The closer the strike price is to the underlying asset value, the higher the risk and the larger the potential rewards. But of course, if the strike price is close to the underlying asset price, then the chance that the underlying asset price hits the call price and the contract is terminated is also higher.

This amplification of risk and reward is known as "gearing". The CBBCs that rise or fall in value faster relative to their underlying asset are more highly geared than the CBBCs that rise or fall more slowly. In our example, the CBBC with the strike price of 10,000 is less highly geared than the CBBC with the strike price of 14,000. More gearing means more risk and more potential rewards.

So like all derivative products, you can make and lose money with CBBCs fast. But you can only lose what you invest in the first place. With a highly geared CBBC this could happen quickly, but these are not designed to be long-term investments. And like all derivatives, CBBCs and their risks are complicated.

If you are considering this product, take this article as a starting point, type every term and every phrase into Google, go talk to your broker and grill him or her on how CBBCs work. Then pick a few CBBCs that suit you and read all the details.

Once you have done all that, if you understand it and you like the risk/reward balance, go for it. But if anything seems confusing, it is a good sign this is not the product for you.

Article posted with the permission of the South China Morning Post.