What is an annuity?

An annuity is a long-term insurance product. It is not a bank deposit, nor a savings plan.

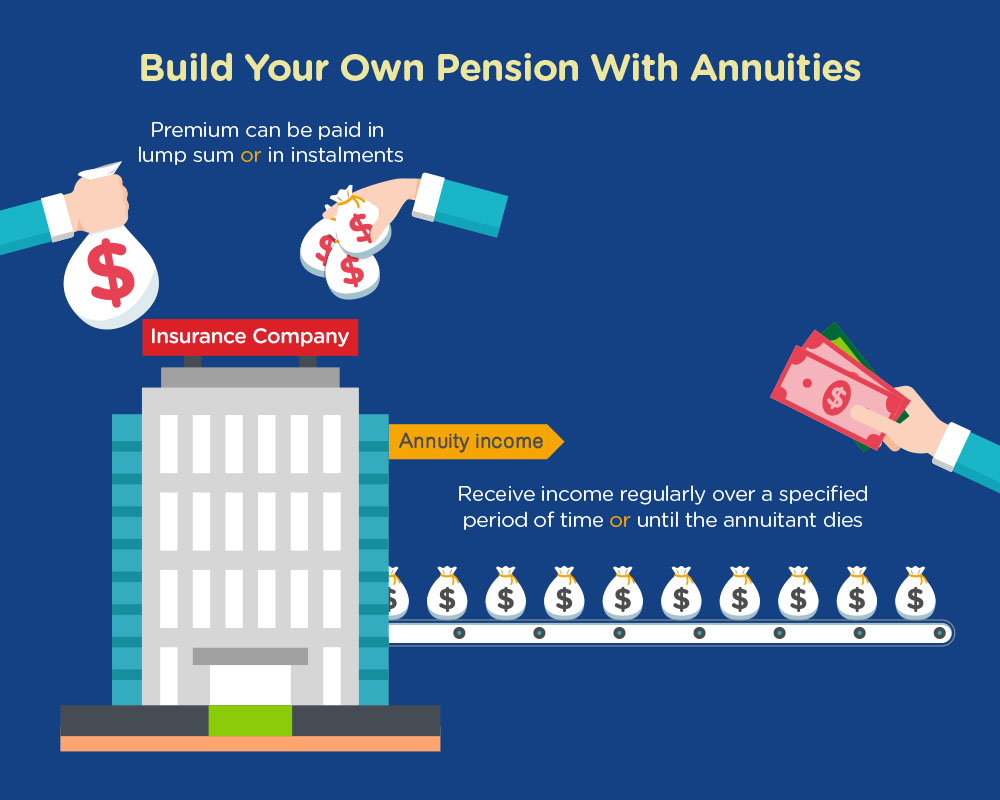

The purpose of an annuity is to help policyholders convert their money into a steady stream of income over the long term. It helps consumers spend their retirement savings in a disciplined way to address the financial risks brought about by longevity. The basic concept is rather simple: the policyholder pays the premium (in a lump sum or in instalments) to an insurance company which will provide regular annuity income to the policyholder immediately or after a designated period of time or after a certain age of the policyholder, for the period specified in the contract. Since this kind of product allows the policyholder to take out cash annually (or monthly / quarterly), it is known as an "annuity". The general public sometimes also refer to an annuity as a "self-made pension".

Learn more: Which type of annuity plan suits me?

Death benefit

In the unfortunate event that the insured passes away, the death benefit would be determined by the time of death occurred, whether during the premium contribution period or the income period. In the case of the contribution period, the beneficiary can usually receive no less than the paid premium in full as death benefit.

In the case of the income period, different arrangements or options would be available under different plans. For example:

- On behalf of the policyholder, the beneficiary can continue to receive the remaining unpaid annuity income until the end of the income period or the guaranteed period; or choose to immediately get back a death benefit in a lump-sum (e.g. all the premium paid less the cumulative monthly annuity payments paid).

- The beneficiary will receive a lump sum according to the death benefit value or cash value of the policy.

- With some annuity policies, there is no remaining value once the insured passes away. In other words, there is no death benefit. This type of annuity is called a pure annuity.

Generally, if the insured passes away after the end of the income period or the guaranteed period, there will not be any death benefit.

Early surrender may incur loss

An annuity is a long-term insurance product. The premium contribution and the income periods can span across decades. Similar to other long-term insurance products, early surrender or termination of an annuity plan may incur financial loss. The surrender or termination value could be much less than the total premiums paid. People who intend to purchase an annuity plan should collect more information and understand the features and risks of these products. They must ensure that they can afford to pay the premium in full, and reserve adequate cash for daily and contingency expenses.

Consumers (especially the elderly) should not use all of their savings to purchase annuities. In the event that a customer realises that an unsuitable plan has been purchased, the consumer has the right to cancel the policy during the cooling-off period, which is within the 21 days after the policy is delivered to the policyholder or his / her representative, or a notice (informing the policyholder that the policy is available and notifying the expiry date of the cooling-off period) is issued to the policyholder or his / her representative, whichever is earlier. If you have any questions, please seek professional advice.

Education materials jointly developed by the IFEC and the Insurance Authority

21 December 2018