Financial planning primer

Common misconceptions about financial planning

Financial planning is a commonly used term, but what does it really mean? Some common misunderstandings about financial planning include:

- One only needs to start financial planning when approaching retirement.

Financial planning is a life-long project; the earlier you start financial planning, the sooner you can enjoy the benefits. A longer investment horizon will also help mitigate short-term volatility risks of the investments. - Financial planning is just another name for investing.

Financial planning is more than just investment. Rather, it's about the big picture bringing together all aspects of personal finance to achieve your financial goals, eg getting married, setting up a home, having children, retirement, starting a business, etc. - Once you finish your financial plan, you don't have to think about it again.

Financial planning is not a one-time deal! You should revisit and review your financial plan regularly to make sure you're on the right track towards achieving your goals as and when your circumstances have changed. - You need a lot of money to do financial planning.

Financial planning is everyone's business, not just for multi-millionnaires. No matter how much income or savings you have, you can always benefit from having a clear plan for your finances. Making and sticking to a financial plan can help you grow your finances and achieve your financial goals.

What is financial planning?

Financial planning is the process of setting, planning, achieving and reviewing your life goals through the proper management of your finances. It involves managing your present and future finances.

A holistic financial plan not only involves investing money and building your wealth; but also your credit and tax obligations, everyday spending, planning for wedding, setting up your home, saving for education fund for your children, saving for your retirement, as well as protection for you and your family through buying suitable insurance policies and conducting estate arrangement. All these facets of your financial plan are interconnected.

Financial planning is an important life skill to help you plan for your future and take better control of your financial goals by helping you to set realistic plans, evaluate alternatives and take effective measures. Prudent financial planning helps you to:

- Satisfy today's financial needs

Can you balance your monthly expense? Do you spend over your limits? Do you often spend on credit cards and do you have credit card indebtedness? Use our budget planner to plan and monitor your savings and expenses. - Meet future financial goals

What are your financial goals, going for vacation, buying a house, getting married? Are these goals realistic under your financial position? Our savings goal calculator may be able to help you plan ahead. - Save for emergencies

No one thinks that they really need to take a step back when everything is good. Do you have enough financial cushions or contingency funds for example saving for three to six months of living expenses to deal with any unexpected crisis? - Protect you and your family in the event of something going wrong

Financial planning involves having the right insurance in place to protect you and your dependents if something goes wrong with your health or with your property; and conducting estate arrangement. - Plan for your retirement

Have you assessed your retirement needs and estimated the future value of your retirement savings including MPF/ORSO/other retirement schemes plus your other savings and investments? Do you need building up your wealth through savings and long-term investments to meet your retirement needs?

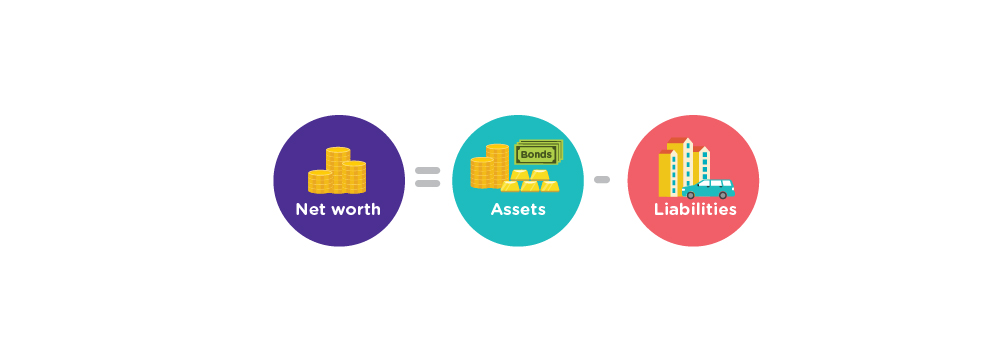

A good starting point for your financial planning process is to gain an accurate understanding of your current financial position, including your net worth.

Net worth is broadly calculated as your assets minus your liabilities. Asset is what you own, including, savings, property, investments; and liability is what you owe, such as mortgage loan, tax bills and outstanding debts.

Through sound money management and investments, you build your savings which contribute towards your assets. Channels of asset or money outflow include consumption from daily living expenses to future life events such as getting married, having children, illness, or becoming unemployed. In terms of the money you can spend and live upon, you may carve out from your net assets, the estate you want to pass down to offspring, family members or donate to charity.

Getting started with financial planning is important because it gives you a plan to achieve your financial goals. A solid plan can help you:

- Determine your strategy for achieving your financial goals.

- Give you better control over your financial future.

- Lead a lifestyle that you pursue while saving for retirement.

Sounds difficult? It doesn't have to be! You can start putting together a basic financial plan all by yourself.

Components of basic financial plan

When putting together your basic financial plan, make sure to consider the following:

- Responsible borrowing: Responsible borrowing is an integral part of financial planning. Personal loans and credit eg mortgage loan and car loan can help you achieve your financial goals, but over-indebtedness can jeopardise your life plan. Many people use credit cards for their day-to-day living and paying by credit card is convenient and easy. The key thing is to make sure you are in control of credit, not the other way around. Your past credit record may also affect your cost of borrowing in the future. Learn more about borrowing.

- Managing day-to-day finances: Managing your money with an effective budget planner helps you identify where you can set aside funds to build your savings while tracking down your expenses. At the same time, you can put your money to work by investing in stocks, bonds, funds, property and many other asset classes, in line with your risk appetite and investment horizon to help meet your financial needs.

- Future consumption: Future consumption includes life events such as further study, getting married, purchasing property, having children, supporting your parents, changing careers, starting your own business or retirement. These expenses may deplete your assets and can be long-term financial commitments.

Beware of anything that might affect the cost of financing and your income in the future, for example, changing jobs or becoming unemployed, the impact of interest rate rise on the monthly interest payments for floating rate loans eg mortgage loans, etc. - Insurance: Unexpected incidents or emergencies in life such as accidents, illness and death can deplete your savings and erode your assets. Risk management is a key component of overall financial planning. Insurance gives you some financial protection against unforeseen circumstances and risks in life.

When considering your insurance needs, some key steps include determining what insurance cover you need and shop around to choose an insurance policy that meets your needs. Learn more about how insurance works.

For better understanding of financial planning and your options, it may be helpful to seek professional advice from a financial planner.