Learn more about tax loans

In September or October every year, the employed population will receive a white envelope from the Inland Revenue Department, containing a salary tax bill with payment details to be settled in the upcoming January. During this time, banks and finance companies begin marketing their tax loans. In recent years, the tax loan market has been bustling with activity. Many banks and finance companies aggressively push their tax loan products to vie for bigger market share.

Interest rate may not be as enticing as advertised

When it comes to tax loans, most people would first associate them with low interest rates because many tax loan commercials highlight so. Tax loans are often promoted offering at an annualised percentage rate, which can be as low as 1.5%, or even with "zero interest". While it is true that interest rates for tax loans are much lower than other personal loans and credit cards, they may not be quite as low as advertised.

The lowest interest rates that are heavily promoted in commercials usually only applies to large loan amounts (e.g. more than $800,000). A higher interest rate is usually imposed on smaller sums.

Besides, the advertised attractive low interest rates may just be applicable for the first few months to draw the attention of customers. If a higher interest rate is applied during the latter part of the loan period, the effective interest rate of the whole term may not be such a good deal after all. Furthermore, "zero interest" loans may charge a handling fee in place of an interest. In other words, "zero interest" does not mean no cost for the loan.

Gifts and rebates may look tempting, but you are actually paying for them. To receive a gift or a rebate, borrowers may be required to meet certain conditions, e.g. apply for a bigger loan amount which means that you will be paying more interest.

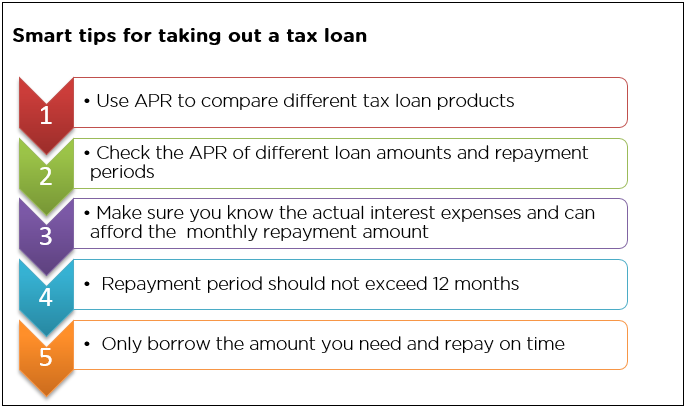

Compare different products with "Annualised Percentage Rate"

Generally, the smaller the loan amount or the longer the repayment period, the higher the interest rate. If you need to apply for a loan to pay your tax, you should check the “Annualised Percentage Rate” (APR) of different loan amounts and repayment periods. An APR is a reference rate which includes the interests and other fees and charges of a loan product expressed as an annualised rate (but does not include charges/interests for late payment and early repayment). The APR facilitates borrowers to compare loan products offered by different banks and finance companies.

Besides, borrowers should keep a clear eye on the monthly repayment amount, take a good look at the actual interest expenses, and assess whether you have the ability to repay the loan. As a general rule, the repayment period of a tax loan should not exceed 12 months, because you will be making your next tax payment same time next year. You can use the IFEC "Borrowing and Debt Calculator" to work out the monthly repayment amount & interest and compare different loan products.

Set up a personal goal

Although the interest rates for tax loans are lower, you can avoid having to take out a loan with early planning and preparation. If you need to apply for a tax loan this year, do set up a goal now and make plans to pay tax without borrowing money next year. You can assume that you will pay a similar tax amount same time next year and use this figure as your savings target. For a more accurate number, use the Inland Revenue Department's tax calculator to compute how much you will be paying. Learn more from Savings made easy with five simple tips. You can also make use of the Government Tax Reserve Certificates to help you save up.