A right product name is important because it helps investors identify a product and understand its features easily.

Like derivative warrants (known as “warrants”) and inline warrants, Callable Bull/Bear Contracts (CBBCs) are derivatives. In the financial market, "bull" and "bear" represent rising and declining trends in the stock market respectively, so the names “Callable Bull Contract” and “Callable Bear Contract” speak for themselves.

CBBCs are always in-the-money

Callable bull contracts, similar to call warrants, are for investors who are bullish on the underlying assets, while callable bear contracts, similar to put warrants, are for investors who are bearish on the underlying assets. While warrants can be in-the-money or out-of-the-money, CBBCs are always in-the-money.

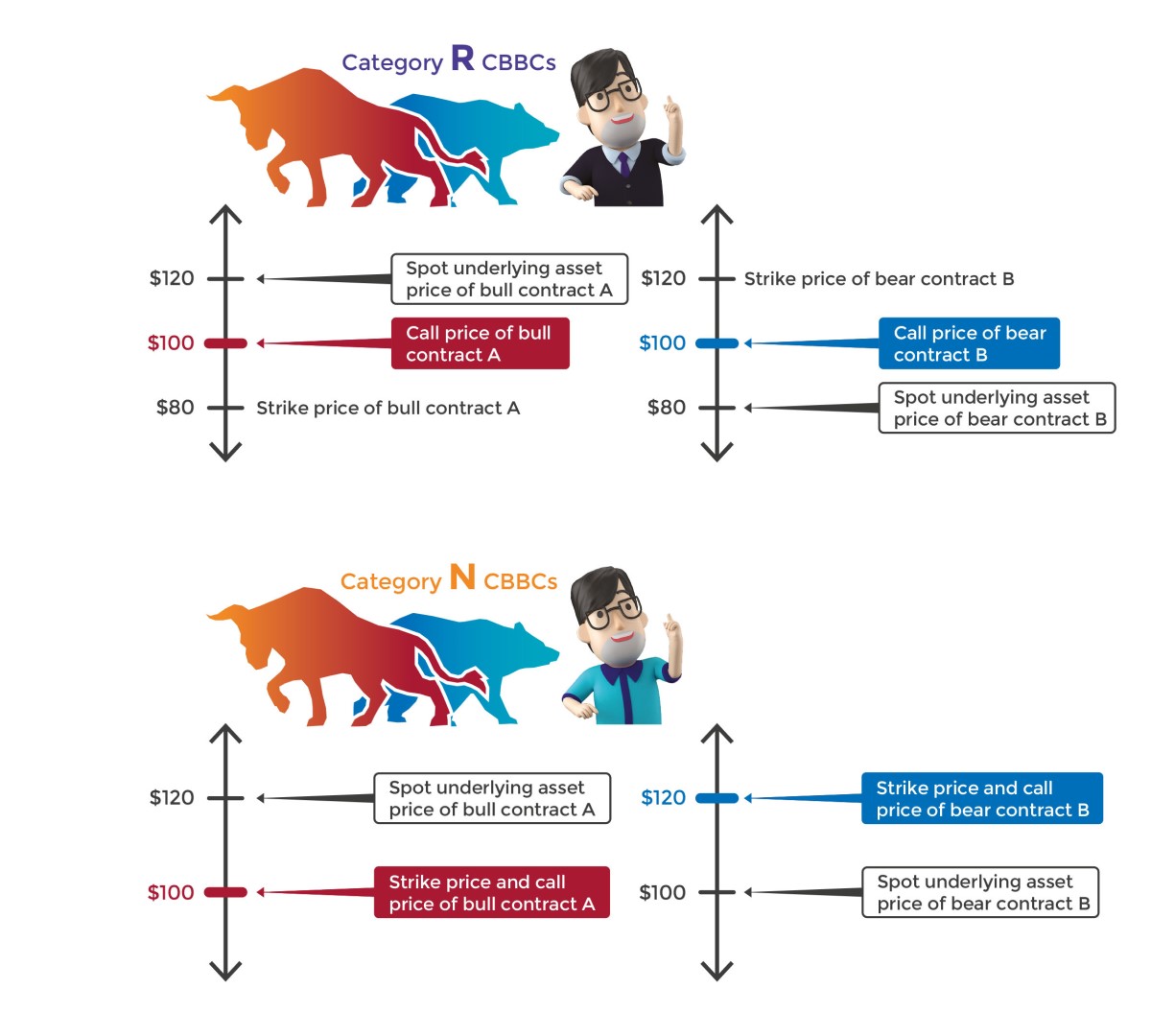

Why? CBBCs have a mandatory call feature measured by reference to a call price (or level if the underlying asset is an index) that is absent in warrants. When the underlying asset price (or level if the underlying asset is an index) reaches or exceeds the call price, the contract will be terminated prior to expiry date. CBBCs are mainly divided into Category R and Category N. Category R CBBCs have different call prices and strike prices (or level if the underlying asset is an index): The call price of a Category R bull contract is above its strike price, while that of a Category R bear contract is set below its strike price. For Category N CBBCs, the call prices are equal to the strike prices. In both R and N categories, the call price and strike price of a bull contract will not be higher than the spot price of the underlying asset, whereas the call price and strike price of a bear contract will not be lower than the spot price of the underlying asset. Hence, CBBCs are always in-the-money.

For bull CBBCs, if the mandatory call event has not triggered, and the closing price of the underlying asset at expiry (or the future contracts settlement price, if the CBBC is linked to index) is higher than the CBBC’s strike price, investors will receive a cash payment, which is calculated by reference to the difference between that closing price and the strike price, adjusted by the conversion ratio. On the other hand, if the closing price of the underlying asset at expiry is equal to or lower than the strike price, the CBBC will become worthless.

For bear CBBCs, if the mandatory call event has not triggered, and the closing price of the underlying asset at expiry is lower than the CBBC’s strike price, investors will receive a cash payment, which is calculated by reference to the difference between the strike price and that closing price, adjusted by the conversion ratio. On the other hand, if the closing price of the underlying asset at expiry is equal to or higher than the strike price, the CBBC will become worthless.

CBBCs vs warrants

With the call price and mandatory call feature in place, the pricing strategy of CBBCs is also different from that of warrants, such as:

No time decay

The mandatory call feature of CBBCs means that the expiry date is not very important as investors usually trade them within a relatively short period of time. Due to its “in-the-money” nature, the value of CBBCs mostly come from their intrinsic value, i.e. the difference between the underlying asset price and the strike price. Hence, the idea of time decay does not apply to CBBCs.

Theoretical price of a CBBC = intrinsic value + financial charges

Intrinsic value of a bull contract = underlying asset price - strike price

Intrinsic value of a bear contract = strike price – underlying asset price

Financial charges (which include the issuer’s costs in relation to CBBCs issuance) are included in the spot price of the CBBC. Financial charges may vary from time to time and will gradually decrease as the contract approaches its expiry date.

Insignificant impact of implied volatility

While implied volatility reflects the likelihood of warrants becoming in-the-money, and is an important factor affecting the price of a warrant. However, as CBBCs are always in-the-money, implied volatility is therefore of lesser importance to the price of CBBCs.

Other factors affecting the price of a CBBC

| Bull contract | Bear contract | |

|---|---|---|

| Underlying asset price ⬆ | ⬆ | ⬇ |

| Dividend of the underlying asset ⬆ | ⬇ | ⬆ |

| Interest rate ⬆ | ⬆ | ⬇ |

22 January2021