What is a qualifying deferred annuity policy (“QDAP”)?

Qualifying Deferred Annuity Policy

For relevant premiums to qualify for tax deductions, a deferred annuity product must comply with the guideline issued by the Insurance Authority, including:

- Minimum total premiums of $180,000 and minimum payment period of 5 years

- Minimum annuity period of 10 years

- Annuitization at the age of 50 or beyond

- Disclosure of the internal rate of return of the product to facilitate evaluation and comparison

- Clear presentation of the guaranteed and non-guaranteed annuity payouts

- Clear separation of premiums of all riders (e.g. critical illness, hospitalisation cash, etc.) from the qualifying deferred annuity premiums

To facilitate filing of tax returns for policyholders, insurance companies will issue an annual summary of QDAP to policyholders every year.

The sales document of a QDAP is printed with the QDAP logo. From 1 April 2019, the public can visit the website of the Insurance Authority (www.ia.org.hk) for the list of QDAP available in the market.

What is an annuity? What is a deferred annuity?

Annuity is a long-term insurance product. The key purpose is to help a policyholder to convert savings into a steady stream of income. A policyholder pays premiums to an insurance company, which in turn, provides him with regular annuity payouts immediately, or after a designated period of time, until he/she reaches a certain time specified in the insurance contract. Annuities can generally be categorized into immediate annuities and deferred annuities.

An immediate annuity does not have an accumulation phase. A policyholder starts receiving annuity payouts monthly once the premium has been paid in a lump sum. For example, the Government-initiated “HKMC Annuity Plan” is an immediate annuity. An immediate annuity is more suitable for retirees as they usually have accumulated a sum of money but have no income. Retirees can use part of their savings to purchase an immediate annuity and start receiving a steady stream of income. Purchasing an annuity only requires a one-off transaction and a policyholder does not need to spend much time managing the annuity in the future. It is a simple retirement financial arrangement that offers peace of mind, particularly for the elderly who are not good at financial management.

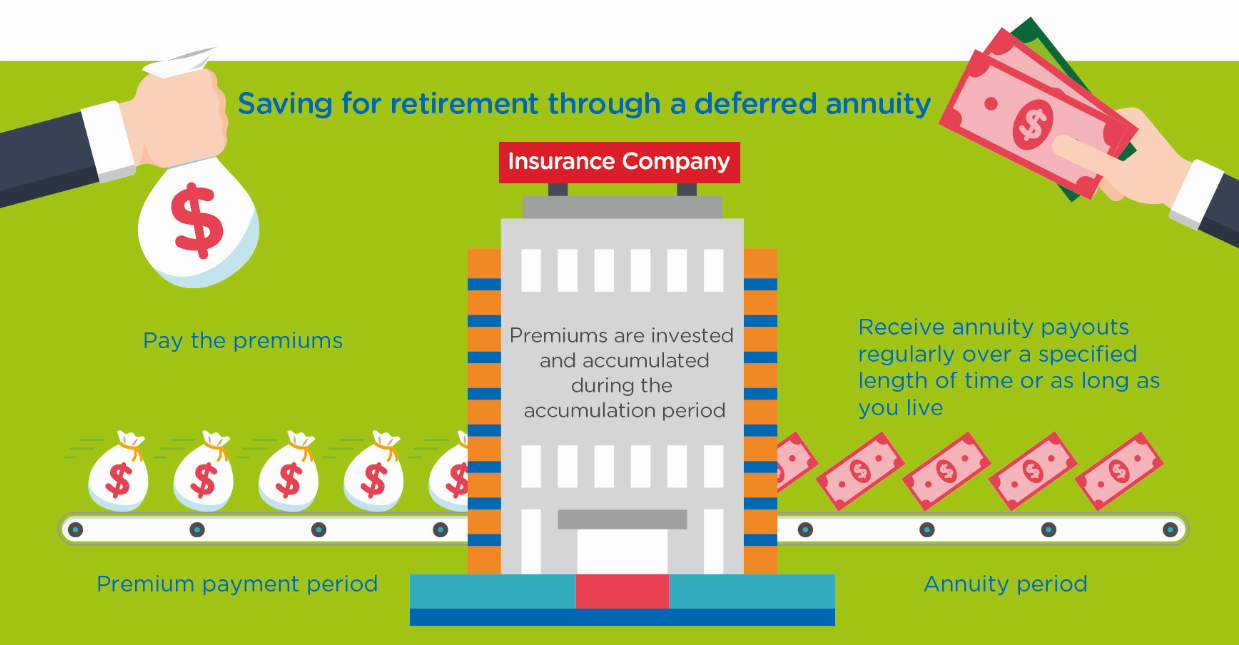

Deferred annuity has an accumulation phase. A policyholder can pay premiums by a lump-sum or by instalments, which are then invested and accumulated during the accumulation phase. A policyholder will start receiving the annuity payouts after a certain period of time (e.g. on retirement). Deferred annuity is more suitable for the working population. It allows policyholders to accumulate retirement savings by instalments when they are young, and convert the savings into a steady stream of income when they retire to cover their daily expenses. Additionally, qualifying deferred annuity premiums are eligible for tax deductions.

Annuity plans offered by the private sector are mostly deferred annuities, with the annuity payouts usually comprising both "guaranteed" and "non-guaranteed" payouts. The “non-guaranteed” part is often affected by factors such as investment returns, claims and profits of the insurance company. In an extreme case, the “non-guaranteed” part can be zero.

Same as other long-term insurance products, early surrender or termination of an annuity plan may incur financial loss. The surrender value could be much less than the total amount of premiums paid. Before buying an annuity, you should consider your liquidity needs and make sure you can afford the premiums over the whole payment period and set aside sufficient cash for daily and contingency expenses. Also, there is usually no remaining value after the end of the annuity period. Individuals who want to leave an inheritance should make other arrangements. Please visit the Annuity Sitelet jointly developed by The Chin Family and the Insurance Authority for more information.