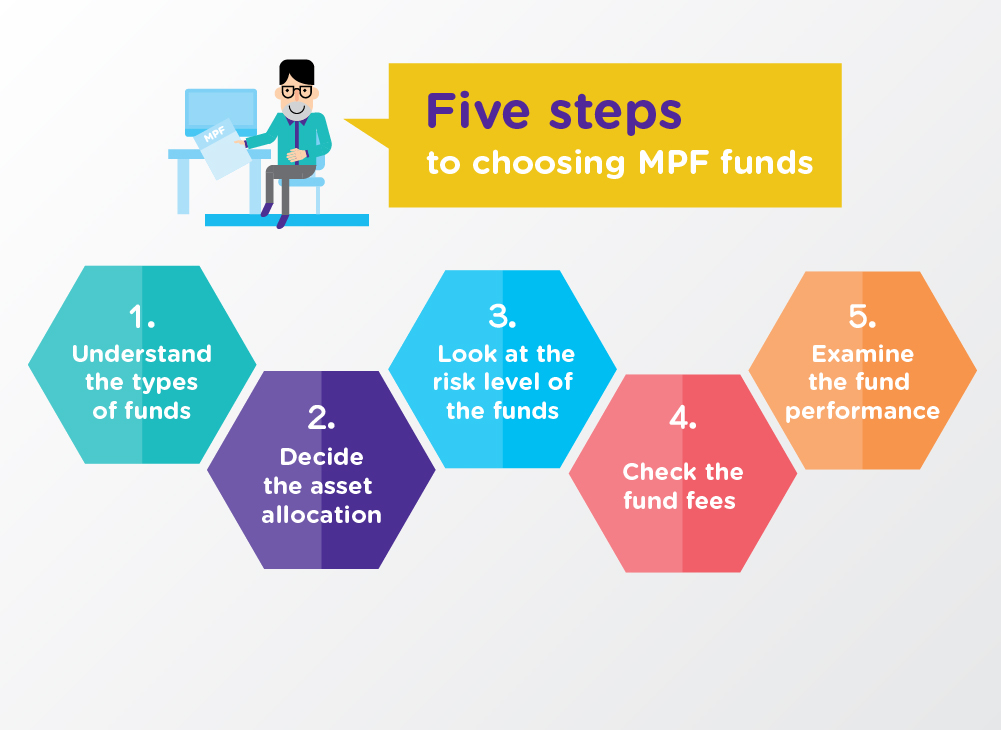

Five steps to choosing MPF funds

The Hong Kong working population makes MPF contributions every month, which form part of our retirement savings. How much do we actually know about our MPF investment?

Some people are confused about MPF fund choices and some may simply give up making a choice. However, your decisions will have an important impact on your savings outcome. Selecting MPF funds isn't as difficult and complicated as you think. Consider the below five steps to choosing MPF funds:

Step 1 - Understand the types of funds

Currently, there are five major types of MPF funds for scheme members to choose from, i.e. equity funds, mixed assets funds, bond funds, guaranteed funds and MPF conservative funds. Understanding their features and risk levels is the first step in choosing MPF funds. In general, the higher the expected return of the fund, the higher the potential risk.

See the features of different types of funds

Step 2 - Decide the proportion of equities, bonds and other assets in your portfolio

Generally speaking, MPF benefits will be withdrawn when you reach the age of 65. If you are young, your investment term may be up to 30-40 years which gives you more time to mitigate the impact of short-term market fluctuations. Therefore, you can consider taking a greater risk. As such, putting a larger share of your money into equities may help to achieve capital gain and counter the risk of inflation. On the contrary, if you are in the middle-age group, you should lower the risk by reducing the portion of equities and holding more bonds or other low-risk assets in the investment portfolio. In addition, diversification across regions or asset classes tends to lower investment risk.

After deciding the asset allocation, you can start to choose MPF funds. The risk level of the funds, fees and performance are the key aspects that you can consider.

Step 3 – Look at the risk level of the funds

Some funds have a higher level of risk as compared with others even if they belong to the same asset class. Using equity funds as an example, sector equity funds are generally riskier than other types of equity funds. Also, putting all your money into a single market equity fund (for example Hong Kong equity fund) will involve higher risk compared with a global equity fund which spreads the investments across different markets. You can refer to the Risk Indicator in the Fund Fact Sheet to choose funds that suit your risk tolerance level.

Step 4 - Check the fees of the funds

The level of fees will have significant impact on the net investment return, in particular that MPF is a long term investment. For example, the Fund Expense Ratio of equity funds ranged from 0.65% to 2.64% (as of Dec-end 2017). In general, the fees of passively managed funds (like index funds) will be lower than actively managed ones.

Step 5 – Examine the performance of the funds

Past performance of a fund is not an indication of its future performance. But it is still useful to understand how the fund performed in the past, in particular, whether it performed consistently well in a long period of time. You can find the performance information in the Fund Fact Sheet.

You can make use of the MPFA’s MPF Fund Platform which provides short/medium/long term fund performance data, Risk Indicator and Fund Expense Ratio to facilitate easy comparison of different MPF funds.

Bear in mind that fund performance can only serve as a reference and you should never choose a fund solely based on its past performance. Refer to the Fund Fact Sheet to understand the fund's features, objective, risk level, fees etc to make sure the fund is suitable for you.

Having chosen the funds that meet your needs does not mean that you no longer need to monitor your MPF account. You should regularly review your fund choices, say once every six months or once a year and make adjustments when necessary.

Default Investment Strategy

Scheme members who do not make their own choice of MPF funds, will be invested according to the Default Investment Strategy (DIS) of their respective scheme. Scheme members can also actively select the DIS if they wish. Check our article MPF Default Investment Strategy at a glance to learn more.